Home loans top the secured loan segment of a bank’s retail book. To

address the needs of various customers, banks usually come up with variations of

home loans, such as fixed-rate loans, floating-rate loans, fixed-floating loans,

etc. But did you know that there is yet another category of home loans wherein

your surplus funds can be linked to the home loan to reduce the equated monthly

instalment (EMI) outgo? Here is how such a loan works and what it means for

you.

What’s on offer?

To avail this product, you have to link a current or a savings

account to your home loan at the same bank. You can deposit any surplus funds in

this linked account. Whenever you deposit a surplus amount in the account, the

bank considers this amount and deducts it from the principal of your home loan

while calculating the interest on the outstanding home loan.

As of now, only a few banks offer this product. These include State

Bank of India, IDBI Bank Ltd, Hongkong Shanghai Banking Corp. (HSBC), Citibank

and Standard Chartered Bank.

Interest rates on such “interest-saver home loans” are usually

higher than that of normal loans—0.5-1.0 percentage points more. For instance,

HSBC, on its website, states that interest rate on normal floating rate home

loan for up to Rs.50 lakh loan amount is 10.75% per

annum. However, interest rate for smart home loan for the same amount is 11.00%

per annum. Similarly, IDBI Bank charges a higher interest rate on interest-saver

loan. Its usual home loan interest rate is currently at 10.25%, but 10.50% for

the interest-saver loans. State Bank of India, which calls this product SBI

Maxgain, charges 0.25 percentage points over the applicable home loan interest

rate for home loans above Rs.1 crore, the bank

states on its website.

How does it work?

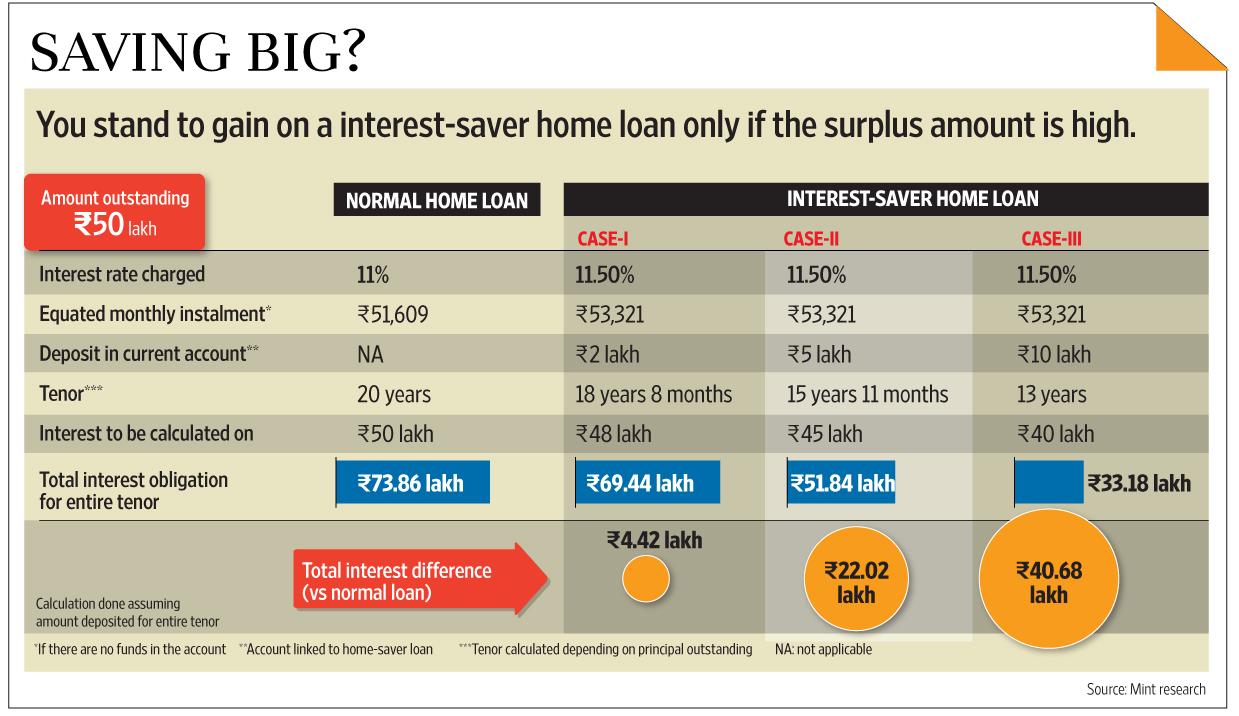

Let’s say you take a Rs.50 lakh home

loan. Now assume you have a surplus amount of Rs.5

lakh. Instead of prepaying the excess amount, deposit that money in a savings

account that is linked to your home loan account. Once you do that, the interest

obligation would be calculated on the loan outstanding less Rs.5 lakh (this is Rs.45

lakh), and not on the entire loan outstanding.

Another benefit is that you can withdraw this money or a part of it

whenever you want. Now if you don’t have money in your savings account, even

when you deposit a recurring amount in your account, this deposit will still be

subtracted from principal outstanding to calculate the EMI. However, if you

don’t deposit money in your account then you will end up paying a higher EMI as

the interest rate is higher than that for normal home loan.

Who should opt for it?

This product has its own pitfalls. Says Adhil Shetty, chief

executive officer, Bank Bazaar, “First, keeping money in a savings or current

account is not profitable. Investors would rather invest in avenues such as

mutual funds, which can give better returns. Second, interest-saver loans are

given at a higher rate than a normal home loan. Banks typically charge 0.5-1.0

percentage points over the normal home loan rates. Calculate the probable

overall savings before going in for such loans. Such loans are good for banks,

too, as the chance of a customer who has a surplus amount defaulting is much

lower.”

Another way of looking at it, adds Shetty, is that your deposit is

earning an interest equal to your home loan interest rate. While these loans

save money, borrowers must also take a wholesome view of the cost associated

with it. You should factor in all the fees and penalties while calculating

benefits. For instance, some banks charge an annual fee of 1% on the outstanding

loan amount for this product. This can be quite expensive.

Another hurdle is that such a loan is not offered by all banks. So,

the only way to avail such loans is to go to a bank that offers it. Borrowers

should also check the eligibility criteria. Says Shetty, “This scheme is useful

for a borrower who has a sufficiently large balance in his account, and also for

a business owner who can park excess funds in his current account. The concept,

though simple, is powerful. The idea is to make use of your deposit in your

current or savings account to offset a part of the principal. Once some of the

principal is offset, interest obligation comes down.”

Now if you are an existing borrower and want to switch to an

interest-saver home loan, first look for the switching charges, which vary bank

to bank. The switching fee can range between 0.5% and 1% of the outstanding

amount. If you compare the surplus amount to a fixed deposit, you will benefit

only if the amount is at a certain threshold.

Says Suresh Sadagopan, a Mumbai-based financial planner, “The bank

is not doing you a favour through this product. For the bank, you are like a

fixed deposit customer. This product treats its customer as a fixed deposit

holder. Only if you deposit money beyond a certain threshold, you will benefit.”

The other problem is the tax treatment of such loans and the

involved amounts. Says Surya Bhatia, a Delhi-based financial planner, “There is

a grey area when it comes to taxation. Considering that you earn an interest

from the money that you deposit in the account against which the loan is offset,

the amount has to be disclosed to the income tax department. There is no clarity

on how it will be shown. Also, the interest-saver home loan product will be

pitched to those who fall in the 30% tax bracket and if they are taxed, the

product will not be worth the while.”

However, even though the interest rate is higher in this product,

the fact that it reduces the tenor will lower your total loan outgo.

No comments:

Post a Comment