A. Introduction:

Through Finance Act, 2018, Central Government has intended to

introduce new scheme of scrutiny assessment under the Income Tax Act, 1961 for

improving effectiveness of tax administration. It has thus brought three new

sections to the Income Tax Act viz. 143(3A) to prescribe new procedure by the

Central Government, 143(3B) to enable Central Government to notify applications

of provisions of the Income Tax Act with such modification, adaptions or

exceptions as may be specified and 143(3C) to provide for laying every

notification issued u/s 143(3A) or 143(3B) before each House of Parliament.

The

intention to implement the faceless assessment was again reiterated by Finance

Minister while presenting budget on 5th August, 2019.

To

effectuate the same, Central Government on 12th September, 2019 brought

notification u/s 143(3A) prescribing the procedure for face-less e-assessment

called as ‘E-Assessment Scheme, 2019’.

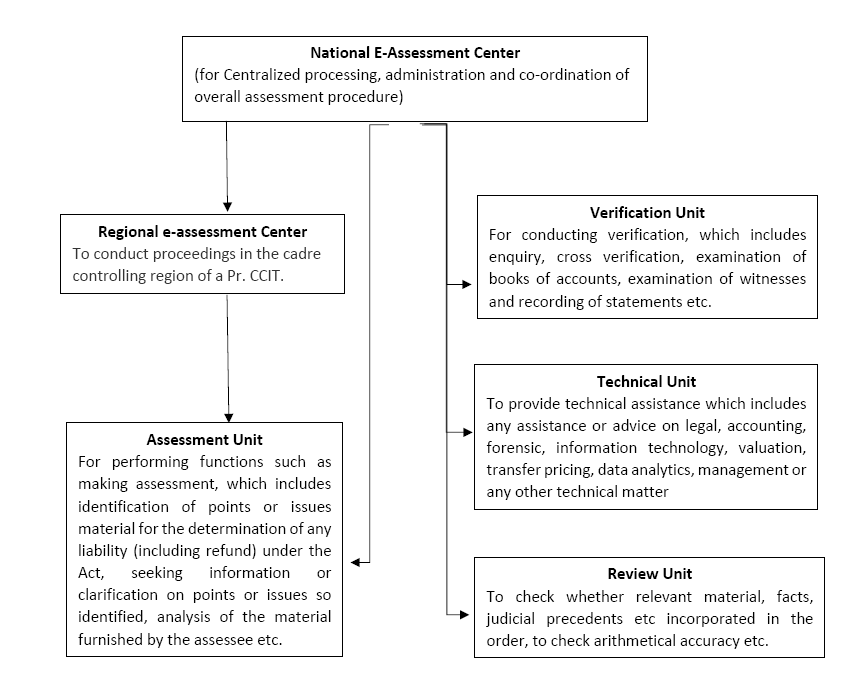

B.

New operational set up:

As per E-assessment Scheme, 2019, following Center and Units

will be constituted to undertake assessment proceedings –

C.

New E-assessment Procedure:

1) A notice u/s 143(2) shall be issued and served by National

e-Assessment Center.

2) Assessee has to file reply within 15 days.

3) The case selected for scrutiny will be assigned to specific

assessment unit or one of Regional e-assessment Center.

4) On request of Assessment Unit, National e-assessment Center

may issue notice for obtaining information, documents or evidence from

assessee.

5) If Assessment Unit request for conducting inquiries or for

seeking technical assistance, National e-assessment Center shall assign said

request to the Verification Unit or Technical Unit respectively.

6) the assessment unit shall, after taking into account all the

relevant material available on the record, make a draft assessment order in

writing either accepting the returned income of the assessee or modifying the

returned income of the assessee along with details of penalty proceedings to be

initiated, if any and send a copy of such order to the National e-assessment

Centre.

7) The National e-assessment Centre then will examine the draft

assessment order in accordance with the risk management strategy specified by

the Board to decide to –

(a) Finalise the assessment as per the draft assessment order

and serve a copy of such order and notice for initiating penalty proceedings,

if any, to the assessee, along with the demand notice or refund due or

(b) In case a modification is proposed in the draft order, it

will provide an opportunity to the assessee by serving a notice calling upon

him to show cause as to why the assessment should not be completed as per the

draft assessment order; or

8) In case modification is proposed, National e-assessment

Center will issue show cause notice to the assessee. If assessee fails to

furnish reply, assessment will be finalized as per draft assessment order

whereas if reply is received, same will be forwarded to Assessment Unit.

9) In case National e-assessment Center assigns the draft

assessment order to a Review Unit in any one Regional e-assessment Centre,

through an automated allocation system, for conducting review of such order,

Review Unit may concur with the draft assessment order or suggest any

modification as it may deem fit.

10) In case Review Unit concur with draft assessment order,

National e-assessment Center will finalize assessment as per point No. 7

whereas in case Review Unit suggests modifications, it will communicate the

same to the Assessment Unit.

11) Assessment unit after considering the modifications

suggested by Review Unit and considering the reply of the assessee in case

proposed modifications are prejudicial to the interest of assessee, shall pass

revised draft assessment order and send the same to National e-assessment

Center.

12) After completion of assessment The National e-assessment

Centre shall transfer all the electronic records of the case to the Assessing

Officer having jurisdiction over such case., for –

(a) imposition of penalty;

(b) collection and recovery of demand;

(c) rectification of mistake;

(d) giving effect to appellate orders;

(e) submission of remand report, or any other report to be

furnished, or any representation to be made, or any record to be produced

before the Commissioner (Appeals), Appellate Tribunal or Courts, as the case

may be;

(f) proposal seeking sanction for launch of prosecution and

filing of complaint before the Court;

13) If considered necessary, National e-Assessment Center at any

stage transfer the case to the assessing officer for completing the assessment

in face to face mode.

D.

Assessments covered:

Since National e-assessment Center can only issue notice u/s

143(2), the assessments initiated by issuing notices under sections other than

section 143(2) such as in following cases may not be covered by this scheme –

a) Where reopening of assessment is initiated by issuing notice

u/s 148;

b) Assessment is taken up in pursuance of search and seizure u/s

153A or 153C; or

c) In case no return is filed despite having taxable income

leading to best judgement assessment u/s 144;

d) Fresh or modified orders for giving effect to the order of

appellate authorities.

E.

Penalty proceedings:

In case assessee fails to comply with notices issued by any

unit, such unit may recommend initiation of penalty proceedings. In such case,

National e-assessment Center will issue show cause notice to the assessee and

if satisfied may drop the penalty otherwise may levy the penalty by passing

order.

F.

Appellate proceedings:

The appeal against the order passed by the National e-assessment

Unit shall be filed before Commissioner of Income Tax (Appeals) having

jurisdiction over jurisdictional assessing officer.

G.

Authentication of record:

Each communication issued by the Department has to be

authenticated by digital signature whereas communication is by the assessee or

other person, it may also be authenticated by electronic verification

techniques such as EVC etc.

H.

Delivery of Notice:

Every notice or order or communication shall be delivered by way

of sending copy to registered account or registered email of assessee or

authorized representative or uploading copy on assessee’s mobile app with real

time SMS.

I.

Use of video conferencing only:

In case any modification is proposed in the draft assessment

order after issuing show cause notice, the assessee or his authorized

representative can seek personal hearing and, in such case, said hearing shall

be exclusively conducted through video conferencing.

It is also clarified that all the statements except statement

u/s 133A would be recorded exclusively through video conferencing.

J.

Open issues:

Though this scheme is laudable effort taken by the government

for hassle free assessment, following aspects needs further clarification or

consideration –

1) This Scheme to the extent inconsistent with the provisions of

section clause (7A) of section 2, section 92CA, section 120, section 124,

section 127, section 129, section 131, section 133, section 133A, section 133C,

section 134, section 142, section 142A, section 143, section 144A, section

144BA section 144C and Chapter XXI of the Act, modifies application of these

sections in its present form. Since this scheme is brought by way of

notification deriving power u/s 143(3A) and 143(3B) by Central Government, its

scope as a delegated legislation can be questioned on the grounds of

substantive ultra vires and on the ground of the constitutionality of the

provisions of the delegated legislation or on the ground of its being

unreasonable and arbitrary.

2) In case matter is referred by National E-Assessment Center to

Review Unit, it may accept the draft order or it may suggest modification.

However, it is not clear whether the modification suggested by the Review Unit

is binding on the Assessment Unit or it may take its own view as the words used

in the scheme are Assessment unit shall consider and not incorporate the said

modifications in the revised draft assessment order.

3) It is not clear as to how the revisionary jurisdiction u/s

263 by the Administrative Commissioner would be exercised? This scheme may

result into dilution of provisions of section 263 as substantial application of

mind is involved in the entire new process.

4) The E-assessment scheme prescribes forwarding of draft

assessment order to National e-assessment Center by Assessment Unit. Since this

scheme modifies inter alia section 92CA and section 144C, it is not clear

whether the National e-assessment Unit will forward draft assessment order to

the assessee giving an option to approach DRP? Presently, it provides no option

to the assessee to raise any objection thereon before DRP. This aspect needs

clarification.

5) It is also not clear as to how the scope of limited scrutiny

will be converted into complete scrutiny during the course of assessment

proceedings by taking approval of Commissioner be implemented under new

E-assessments regime.

6) How the satisfaction as required u/s 14A, 68 to 69C etc will

be recorded? Will it be recorded by Assessment Unit or can also be directed by

Review Unit or National E-assessment Center?

7) It is not clear whether Assessment Unit or jurisdictional

assessing officer will invoke provisions of General Anti Avoidance Rule.

K.

Conclusion:

By bringing E-assessment Scheme, 2019 Government has taken one

more step towards ‘minimum government maximum governance’ with optimally using

technology for achieving Digital India initiative. It is a great step taken by

the Central Government to impart greater transparency and accountability by

eliminating the interface between the Assessing Officer and the assessee and by

effectively utilizing the resources through introduction of team-based

assessment. It may also strengthen the quality as well as uniformity of

assessments as specific assessment unit will be handling the cases selected for

specific reason for e.g. penny stock cases may be handled by one particular

assessment unit. However initial period may seem some transitional issues which

hopefully government will solve with further clarification and streamlining the

processes.

No comments:

Post a Comment